The Choke-Chain Effect: Capitalism Beyond Rapid Growth

March 14, 2019

The economies of early industrialized countries have left the time of rapid growth behind. One of the reasons for this end of rapid economic growth in these countries is a trend towards tightened profits that James Galbraith has called “the choke-chain effect”.

The term describes the fact that the resource- and energy-intensive economy that emerged after 1945 in East and West alike, which ensured prosperity through high growth rates, cannot continue unchanged because the efficiency of such an economic type can only be increased as long as resources remain cheap. However, resource intensity also means high fixed costs, which amortize only over a long period of time. These costs can only be justified if the system is expected to remain profitable over a longer time. Political and social stability is therefore a central functional condition of this type of economic activity. Because of their stability requirements, high fixed cost systems are particularly vulnerable. But what happens when times become uncertain and commodity and energy prices rise? The time horizon for profits and investments is reduced, and the total surplus or profit of a company is lower than in stable times. Because profits are shrinking, distributional conflicts on all levels – between workers, management, owners, and tax authorities – are intensifying because confidence in a positive development begins to waver.

This “choke-chain effect” further intensifies if (a) there is a scarcity of a crucial resource, in the sense that aggregate demand exceeds the total supply at the ordinary price, and (b) the supply of that commodity can be manipulated by hoarding and speculation.

Like the choke collar in a dog, the effect does not necessarily prevent economic growth. But as the consumption of energy resources accelerates, prices rise quickly and profitability drops rapidly. This lowers investment, sows doubts about the sustainability of growth and may also trigger a (perverted) tightening of other economic levers.

These considerations do not even cover the high costs of climate change. Commodity and energy costs are not the only causes of the major 2007-2009 crisis, nor are they the sole cause of comparatively low growth rates in the old capitalist centers. However, resource issues, once the cost of climate change becomes acute, could prove a major obstacle to growth. The problem is obvious: To allow organized life on the planet to continue in its present form, massive reductions in carbon emissions will be necessary, and this will be costly; in addition, much of the current energy-consuming business activity would become unprofitable.

Despite the internal economic controversy surrounding this, the analysis is of importance to the discussion of capitalism, growth, and democracy in at least three respects. Firstly, it becomes clear that post-growth societies – more precisely, post-growth capitalisms with relatively weak or no growth in the rich North – have long since become a social reality. The causes for this development are partly structural, partly political. With the conversion of private debt into public debt in order to save banks, the countries of the Eurozone have bought time, but a sustainable solution to structural economic imbalances is not included in the measures taken. The European austerity policy has failed, and even some of its protagonists now admit that, especially in the Greek case.

But Keynesian policies with higher wages and increased demand are not really an alternative. The current proposals overlook the structural power gap that has been further consolidated with the European debt regime. Because financial markets are globally linked and investors assess risks internationally, adjustments in individual countries do not add up to much. In other words, structural obstacles block the way to lasting economic recovery. It is quite possible that in some countries and regions the economy will grow at high rates for a long time, but growth and distribution are becoming ever more uneven, and overall a return to the high growth rates of the past is not expected.

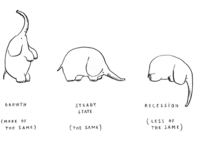

Secondly, if this is correct, it implies that it makes little sense to normatively exaggerate the concept of post-growth society or even reserve it for post-capitalist alternatives. Instead, we need to figure out what slow growth with permanently low growth rates means for the relation between capitalism and democracy. Obviously, capitalist economies can stagnate over longer periods of time (see Japan, Italy) or even shrink (Greece) without any change at the core of their socioeconomic structure. And in its power structures, relatively stable capitalism with weak growth rates is thus possible for longer periods of time – but whether this also applies to the stability of democratic institutions and procedures is another matter.

Thirdly, it also means that while we argue that a return to rapid growth is not possible, a blanket critique of growth and capitalism and the idea of a stagnant or even shrinking economy do not seem to be the way forward. Instead, a consciously slow-growing new economy that incorporates the biophysical foundations of economics into its functioning mechanisms could be a solution. A stagnant or even shrinking economy will always produce few winners and many losers. For these reasons, a kind of economic activity is needed in the future, which could guarantee slow, stable growth over longer periods of time. We suggest a decentralized capitalism with slow growth as desirable. Such capitalism, however, would be significantly different from its financialized varieties. It would have to significantly reduce the size of institutions and organizations (the military) whose fixed costs include an expansive use of resources, and abolish the banking sector as a whole. It would ensure all citizens a decent standard of living, make early retirement possible, raise the minimum wage strongly, relieve the burden of tax on labor but significantly increase inheritance and gift taxes. Most importantly, it would provide incentives to ensure active spending on a socially and environmentally sustainable infrastructure rather than passive accumulation. Whether this is a realistic scenario is an open question.

Sociology must join the search for an answer. An attempt will be made as part of the conference ‘Great Transformation. The Future of Modern Societies’ which will take place at the end of September 2019 in the German university town of Jena. There, we want to launch a research network which will open the possibility for sociologists and economists to participate in a global dialogue on a future beyond rapid growth.

James K. Galbraith, University of Texas, USA

Klaus Dörre, University of Jena, Germany <klaus.doerre@uni-jena.de>